Delving into the world of high net worth advisors and their strategies for tax-efficient portfolios, this guide aims to shed light on the complexities of structuring investments with tax efficiency in mind.

Exploring the intricacies of asset allocation, tax-efficient investment vehicles, tax-loss harvesting techniques, estate planning considerations, and the delicate balance between risk management and tax efficiency, this guide uncovers the key principles and strategies used by high net worth advisors.

Overview of Tax-Efficient Portfolios

Tax-efficient portfolios are investment strategies designed to minimize the impact of taxes on investment returns. By strategically structuring portfolios with tax efficiency in mind, investors aim to maximize after-tax returns and preserve more of their wealth over time.

Importance of Tax Efficiency in Investment Strategies

One of the key reasons why tax efficiency is crucial in investment strategies is because taxes can significantly erode investment returns over time. By minimizing tax liabilities through strategic planning, investors can potentially increase their overall wealth accumulation.

Benefits of Structuring Portfolios with Tax Efficiency in Mind

- Lower Tax Burden: By incorporating tax-efficient strategies, investors can reduce the amount of taxes they owe on their investment gains, allowing them to keep more of their returns.

- Enhanced Returns: With tax-efficient portfolios, investors can potentially achieve higher after-tax returns compared to traditional investment approaches, leading to greater wealth accumulation over time.

- Long-Term Wealth Preservation: Tax-efficient portfolios are designed to help investors preserve their wealth over the long term by minimizing the impact of taxes on their investment gains.

- Diversification Opportunities: Tax-efficient investing often involves diversifying across different asset classes and investment vehicles to optimize tax benefits and reduce overall risk.

Asset Allocation Strategies for High Net Worth Individuals

When it comes to structuring tax-efficient portfolios for high net worth individuals, asset allocation plays a crucial role. High net worth advisors often utilize various asset allocation strategies to optimize tax efficiency while maximizing returns for their clients. These strategies involve carefully selecting and balancing different asset classes based on their tax implications and potential impact on overall portfolio performance.

Comparison of Asset Classes in Terms of Tax Implications

- Equities: Stocks held for over a year are subject to long-term capital gains tax rates, which are typically lower than ordinary income tax rates. Dividends from equities are also taxed at lower rates for qualified dividends.

- Bonds: Interest income from bonds is taxed at ordinary income tax rates, which can be higher than capital gains tax rates. Municipal bonds, however, offer tax-exempt interest income at the federal level and sometimes at the state level, making them a tax-efficient option for high net worth individuals.

- Real Estate: Real estate investments can provide tax advantages such as depreciation deductions, 1031 exchanges for deferring capital gains taxes, and potential tax benefits from rental income.

- Alternative Investments: Hedge funds, private equity, and other alternative investments may have complex tax structures that can impact tax efficiency. These investments often involve various tax strategies to optimize tax outcomes for high net worth individuals.

Impact of Asset Allocation on Tax Efficiency

For example, a high net worth individual looking to minimize tax liabilities may allocate a larger portion of their portfolio to tax-efficient investments like municipal bonds or tax-managed mutual funds. By strategically balancing their asset allocation, they can reduce the overall tax burden on their investment returns.

Tax-Efficient Investment Vehicles

When it comes to structuring tax-efficient portfolios for high net worth individuals, the choice of investment vehicles plays a crucial role. Different investment options come with varying tax implications, and selecting the right mix can help maximize tax benefits.

Tax-Efficient Investment Options

- Individual Retirement Accounts (IRAs): IRAs offer tax advantages such as tax-deferred growth or tax-free withdrawals, depending on the type of account.

- 401(k) Plans: These employer-sponsored retirement accounts allow for tax-deferred contributions and potential matching contributions from employers.

- Municipal Bonds: Municipal bonds are tax-exempt at the federal level and sometimes at the state level, making them attractive for high net worth investors in higher tax brackets.

- 529 Plans: These education savings plans provide tax-free growth when used for qualified education expenses.

Comparing Tax Implications

It is essential to compare the tax implications of different investment vehicles to make informed decisions. For example, while traditional IRAs offer tax-deferred growth, Roth IRAs provide tax-free withdrawals in retirement.

Maximizing Tax Benefits

One strategy for maximizing tax benefits through investment selection is to consider the investor's tax bracket and time horizon. For example, high net worth individuals in higher tax brackets may benefit more from tax-free investments like municipal bonds.

Tax-Loss Harvesting Techniques

Tax-loss harvesting is a strategy used by high net worth advisors to reduce tax liabilities within a portfolio. This technique involves selling investments that have experienced a loss to offset capital gains and potentially reduce taxable income.

Benefits of Tax-Loss Harvesting

- Reduction of tax liabilities: By strategically selling investments with losses, investors can offset capital gains and reduce the taxes owed on profitable investments.

- Enhanced portfolio returns: Implementing tax-loss harvesting can improve overall portfolio returns by minimizing taxes and increasing after-tax gains.

- Opportunity for rebalancing: When selling underperforming assets for tax purposes, investors can also rebalance their portfolio to maintain their target asset allocation.

Best Practices for Implementing Tax-Loss Harvesting

- Identify suitable investments: Look for assets in the portfolio that have experienced losses and can be sold to offset gains effectively.

- Understand wash sale rules: Be aware of IRS regulations that prevent repurchasing a substantially identical investment within 30 days to claim a tax loss.

- Regularly review and rebalance: Continuously monitor the portfolio for opportunities to harvest losses and rebalance to maintain the desired asset allocation.

- Consider long-term tax implications: Evaluate the impact of tax-loss harvesting on future tax obligations and long-term investment goals.

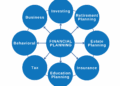

Estate Planning Considerations for High Net Worth Individuals

Estate planning is a crucial aspect of structuring tax-efficient portfolios for high net worth individuals. It involves making arrangements for the transfer of wealth and assets to heirs in a tax-efficient manner, ensuring that the tax burden on beneficiaries is minimized.

Key Estate Planning Tools and Techniques

- Trusts: Setting up trusts can help high net worth individuals protect their assets, control how they are distributed, and potentially reduce estate taxes.

- Gift Giving: Making gifts during one's lifetime can help reduce the size of the taxable estate, thereby lowering potential estate taxes.

- Life Insurance: Life insurance policies can be used as an estate planning tool to provide liquidity for estate taxes and ensure beneficiaries are financially protected.

- Charitable Giving: Donating to charity can have tax benefits and reduce the size of the taxable estate, benefiting both the charity and the estate.

- Family Limited Partnerships: Creating family limited partnerships can help consolidate assets and facilitate the transfer of wealth to future generations while potentially reducing estate taxes.

Risk Management and Tax Efficiency

Risk management and tax efficiency are crucial aspects of portfolio structuring for high net worth individuals. By effectively managing risk and optimizing tax outcomes, advisors can help clients achieve their financial goals while minimizing unnecessary tax liabilities.

Relationship between Risk Management and Tax Efficiency

- Risk management involves assessing and mitigating potential risks that could impact investment portfolios. By diversifying assets, using hedging strategies, and setting risk tolerance levels, advisors aim to protect wealth from market volatility.

- Tax efficiency, on the other hand, focuses on minimizing tax liabilities through strategic investment choices, utilizing tax-advantaged accounts, and implementing tax-efficient strategies like tax-loss harvesting.

- The relationship between risk management and tax efficiency lies in the balance between protecting wealth from potential losses due to market fluctuations while also optimizing tax outcomes to maximize after-tax returns.

Impact of Risk Management Strategies on Tax Outcomes

- Implementing risk management strategies such as asset diversification can help reduce the impact of market downturns on investment portfolios, potentially lowering capital gains tax liabilities.

- Using hedging techniques like options or futures contracts can provide downside protection during market volatility, which may result in reduced tax consequences from selling assets at a loss.

- Balancing risk management with tax considerations can lead to more tax-efficient portfolio construction by optimizing the timing of capital gains realization and leveraging tax-advantaged accounts effectively.

Balancing Risk and Tax Considerations in Portfolio Structuring

- High net worth advisors must carefully weigh the trade-offs between risk and tax implications when structuring portfolios for clients. This involves understanding the client's risk tolerance, investment goals, and tax situation.

- By integrating risk management techniques with tax-efficient strategies, advisors can tailor portfolios to meet both the client's financial objectives and tax optimization goals.

- Regular monitoring and adjustments to the portfolio based on changing market conditions and tax laws are essential to ensure that the balance between risk management and tax efficiency is maintained over time.

End of Discussion

In conclusion, understanding how high net worth advisors structure tax-efficient portfolios is crucial for maximizing returns while minimizing tax liabilities. By implementing these strategies effectively, investors can navigate the intricate world of tax-efficient investing with confidence and success.

Detailed FAQs

What are some common asset allocation strategies used by high net worth advisors?

High net worth advisors often employ a mix of equities, fixed income, real estate, and alternative investments to diversify portfolios and optimize returns while minimizing risk.

How can tax-loss harvesting reduce tax liabilities?

Tax-loss harvesting involves selling investments at a loss to offset capital gains, thereby reducing taxable income and lowering tax liabilities for investors.

What are some key estate planning tools for high net worth individuals?

High net worth individuals may utilize trusts, family limited partnerships, and charitable giving strategies to minimize estate taxes and ensure a smooth transfer of wealth to heirs.

{kind=link}